Stock Portfolio Organizer

The ultimate porfolio management solution.

WiseTrader Toolbox

#1 Selling Amibroker Plugin featuring:

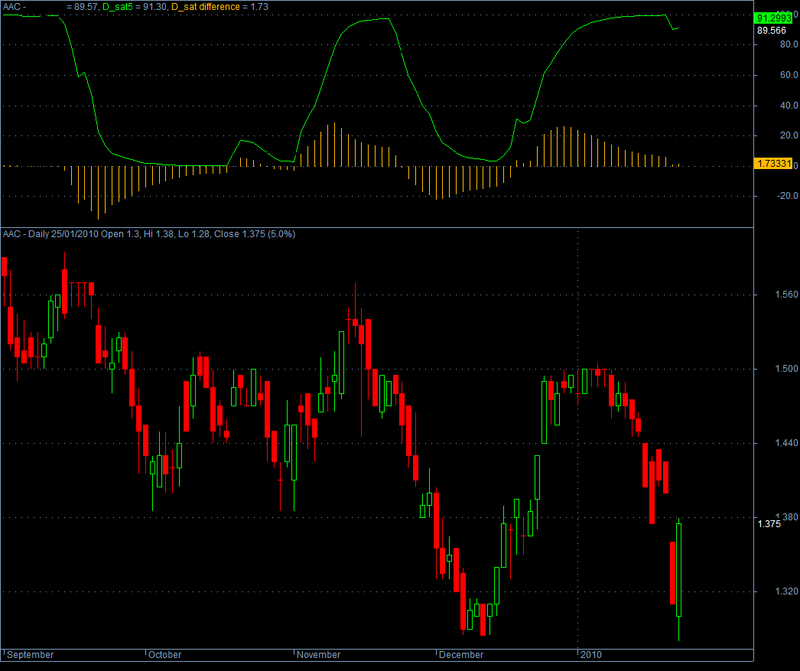

The Saturation Indicator D_sat for Amibroker (AFL)

There are some discrete phases for a bullish trend. The beginning is usually sharp, the market changes direction quickly, Short positions are covered with rush, Long entries may be obliged to follow gap ups etc. The rate of change is becoming slower, premature profit taking appears as long as new buyers are added to the list. Intermediate good market news keep on giving bullish pulses, buyers search for new opportunities not to loose the trend but not to buy expensive shares and this makes a circular money transfer with an always repeated result : The directional movement of the market. When the buying and selling pressure come to some equilibrium, we have the saturation point and this is the end of the main trend. Some stocks may move higher for a while but the market has already prepared the next bearish phase. Last summer I designed a nice indicator giving a graphic emphasis to this saturation phenomena of bullish movements. It is the RSI of the smoothed CMO and it will be called D_sat .

Screenshots

Indicator / Formula

/*The Saturation Indicator D_sat, by Dimitris Tsokakis, Dec 2002*/ P=30; CMO30=100*((Sum(IIf(C>Ref(C,-1),(C-Ref(C,-1)),0),P))-(Sum(IIf(C<Ref(C,-1),(Ref(C,-1)-C),0),P)))/((Sum(IIf(C>Ref(C,-1),(C-Ref(C,-1)),0),P)+(Sum(IIf(C<Ref(C,-1),(Ref(C,-1)-C),0),P)))); C1=DEMA(CMO30,30); D_sat10=RSIa(C1,10); D_sat5=RSIa(C1,5); Plot(D_sat10,"D_sat10",1,1);Plot(D_sat5,"D_sat5",5,1);Plot(D_sat5-D_sat10,"D_sat difference",9,2);

0 comments

Leave Comment

Please login here to leave a comment.

Back